This is what I wrote in # 1561 on 10/23/2023 before the Q3'23 CC

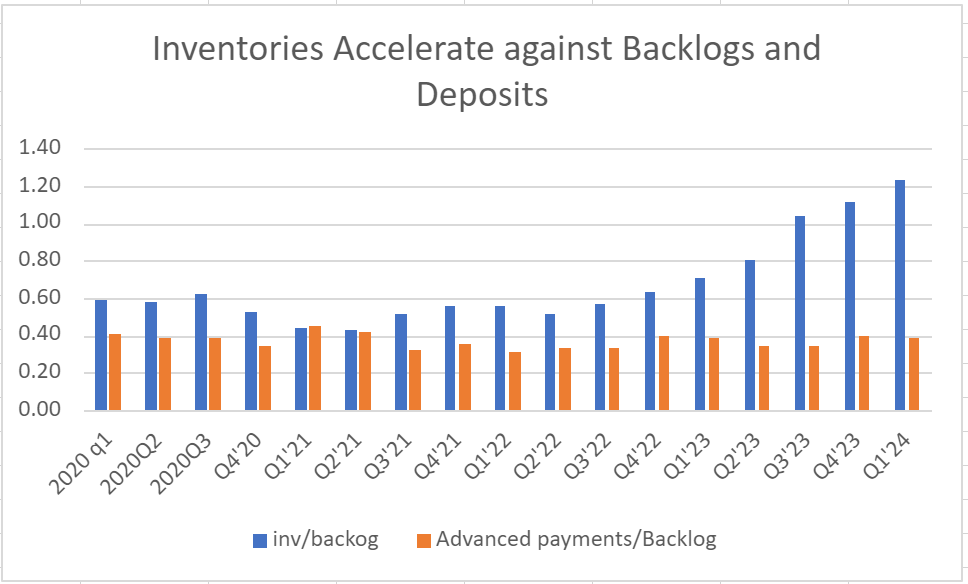

"In this chart I have included the advanced payments/Backlog. The ratio stays pretty constantly in 0.3-0.4, in contrast to the inventories/backlog which ramps noticeably in 2022Q4. I can speculate that Aixtron decided to build inventories without getting the firm orders which would come with advanced payments. Is it because Aixtron anticipated very large orders coming in and wanted to build inventories beforehand? Export licenses cannot explain this because they were largely resolved and shipped in Q2/2023. If Aixtron is building large inventories without the advanced payments, we could expect a very robust Q4 and into 2024. Perhaps Aixtron could clarify in the 10/26 CC."

This is the updated chart after Q1'24. Six month later, the inventories have been getting worse, accelerating against the order backlog and customer deposits (Advanced payments).

The inventories/backlog ratio has moved to 100% higher than its target of 0.5-0.6 provided by Dr. Danninger in the Q1'23 CC.

I hope Aixtron starts turning its huge inventories very soon. Since the Q2'24 revenue would only be 130m (midpoint), a meaningful inventories drop could only occur in H2. That depends on its customers confirming order deliveries by Q3'24.

|

Angeh�ngte Grafik:

screenshot_(39).png (verkleinert auf 52%)

Thread abonnieren

Thread abonnieren

baggo-mh

baggo-mh