Las Vegas Sands - und NUR LSV!

|

Seite 16 von 19

neuester Beitrag: 05.07.23 19:54

|

||||

| eröffnet am: | 22.05.09 13:10 von: | MisterDurden | Anzahl Beitr�ge: | 463 |

| neuester Beitrag: | 05.07.23 19:54 von: | neymar | Leser gesamt: | 100385 |

| davon Heute: | 24 | |||

| bewertet mit 6 Sternen |

||||

1 |

... |

13 |

14 |

15 |

|

17 |

18 |

19

1 |

... |

13 |

14 |

15 |

|

17 |

18 |

19

|

||||

Thread abonnieren

Thread abonnieren

|

--button_text--

interessant

|

|

witzig

|

|

gut analysiert

|

|

informativ

|

0

Optionen

| Antwort einfügen |

| Boardmail an "woblu" |

|

Wertpapier:

Las Vegas Sands

|

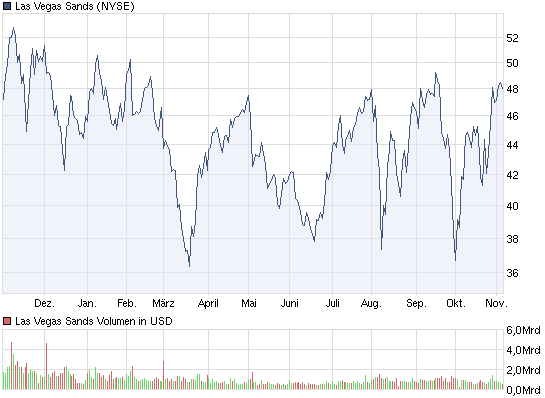

Angeh�ngte Grafik:

chart_year_lasvegassands.png (verkleinert auf 93%)

chart_year_lasvegassands.png (verkleinert auf 93%)

0

Datum Erster Hoch Tief Schluss St�cke

10.11.11 46,24 46,28 43,84 44,56 $ 19.809.800

09.11.11 47,02 47,35 46,04 46,26 $ 11.301.400

08.11.11 47,53 48,17 46,86 48,06 $ 10.851.800

Optionen

| Antwort einfügen |

| Boardmail an "woblu" |

|

Wertpapier:

Las Vegas Sands

|

0

Optionen

| Antwort einfügen |

| Boardmail an "woblu" |

|

Wertpapier:

Las Vegas Sands

|

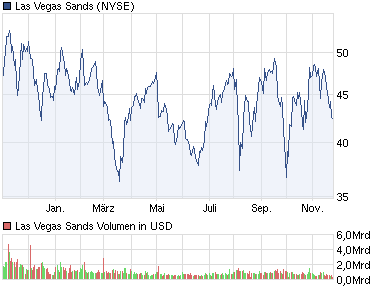

Angeh�ngte Grafik:

chart_year_lasvegassands.png

chart_year_lasvegassands.png

0

Das Unternehmen sagte, es w�rde rund $ 800 Millionen, oder $ 1 pro Aktie, im Laufe des n�chsten Jahres. Chief Executive Sheldon Adelson ist wahrscheinlich mindestens rund 343.000.000 $ aus, dass zu empfangen, nach den neuesten Aufzeichnungen seiner Eigent�merstellung.

"Unsere geografische Vielfalt und die St�rke unserer Operationen in jedem unserer Standorte ... hat uns hier in einer einzigartigen und beneidenswerten ...

Quelle: http://online.wsj.com/article/...82748.html?ru=yahoo&mod=yahoo_hs

Optionen

| Antwort einfügen |

| Boardmail an "Heron" |

|

Wertpapier:

Las Vegas Sands

|

0

16:14 03.02.12

New York (aktiencheck.de AG) - Ryan Worst, Analyst von Brean Murray, Carret & Co, stuft die Aktie von Las Vegas Sands (Las Vegas Sands Aktie) unver�ndert mit dem Rating "buy" ein. Das Kursziel werde von 54 USD auf 57 USD angehoben. (Analyse vom 03.02.2012) (03.02.2012/ac/a/a)

Offenlegung von m�glichen Interessenskonflikten: M�gliche Interessenskonflikte k�nnen Sie auf der Site des Erstellers/ der Quelle der Analyse einsehen.

Quelle: Aktiencheck

Optionen

| Antwort einfügen |

| Boardmail an "Heron" |

|

Wertpapier:

Las Vegas Sands

|

0

Optionen

| Antwort einfügen |

| Boardmail an "Heron" |

|

Wertpapier:

Las Vegas Sands

|

0

Moderation

Zeitpunkt: 23.07.12 08:47

Aktion: L�schung des Beitrages

Kommentar: Löschung auf Wunsch des Verfassers

Zeitpunkt: 23.07.12 08:47

Aktion: L�schung des Beitrages

Kommentar: Löschung auf Wunsch des Verfassers

Optionen

| Antwort einfügen |

| Boardmail an "Atzetrader" |

|

Wertpapier:

Las Vegas Sands

|

0

16:48 22.02.12

Z�rich (www.aktiencheck.de) - Die Analysten der UBS stufen die Aktie von Las Vegas Sands (Las Vegas Sands Aktie) unver�ndert mit dem Rating "buy" ein. Das Kursziel werde von 57,00 USD auf 62,00 USD erh�ht. (Analyse vom 22.02.2012) (22.02.2012/ac/a/a)

Offenlegung von m�glichen Interessenskonflikten: M�gliche Interessenskonflikte k�nnen Sie auf der Site des Erstellers/ der Quelle der Analyse einsehen.

Quelle: Aktiencheck

Optionen

| Antwort einfügen |

| Boardmail an "Heron" |

|

Wertpapier:

Las Vegas Sands

|

0

http://www.finanznachrichten.de/...tanding-6-375-senior-notes-256.htm

--STRONG BUY--

Optionen

| Antwort einfügen |

| Boardmail an "Jennen" |

|

Wertpapier:

Las Vegas Sands

|

0

Forward Annual Dividend Rate4: 1.00

Forward Annual Dividend Yield4: 1.80%

Trailing Annual Dividend Yield3: N/A

Trailing Annual Dividend Yield3: N/A

5 Year Average Dividend Yield4: N/A

Payout Ratio4: N/A

Dividend Date3: Mar 29, 2012

Ex-Dividend Date4: Mar 16, 2012

Optionen

| Antwort einfügen |

| Boardmail an "Heron" |

|

Wertpapier:

Las Vegas Sands

|

0

5-Mar-2012

Regulation FD Disclosure

Punkt 7.01. Regulation FD Disclosure.

Am 2. M�rz 2012 �bte Dr. Miriam Adelson, der Ehegatte von Sheldon G. Adelson, der Vorsitzende und Chief Executive Officer der Las Vegas Sands Corp ("LVSC"), einen Haftbefehl zu 87.500.175 Stammaktien LVSC die zu einem Aus�bungspreis zu kaufen Preis von $ 6,00 pro Aktie bezahlt und LVSC das Aggregat Warrant-Aus�bungspreis von $ 525,0 Millionen in bar. Der Haftbefehl wurde als Teil der Investition, dass Dr. Adelson in LVSC machte im November 2008 ver�ffentlicht. Im Anschluss an die Begebung der Options-Aktien, Dr. Adelson, Mr. Adelson, ihre Familienangeh�rigen und Trusts und anderen Einrichtungen etabliert zu ihren Gunsten wirtschaftlicher Eigent�mer von ca. 52% der ausstehenden Stammaktien LVSC-Aktie.

Die Angaben in diesem Formular 8-K gelten nicht als "abgelegt" werden f�r Zwecke der

� 18 des Securities Exchange Act von 1934 in ge�nderter Fassung, noch gilt sie als durch Bezugnahme in irgendeiner Ablage unter dem Securities Act von 1933 in der geltenden Fassung, au�er wie ausdr�cklich dargelegt werden durch einen entsprechenden Verweis in solch eine Einreichung.

Optionen

| Antwort einfügen |

| Boardmail an "Heron" |

|

Wertpapier:

Las Vegas Sands

|

0

Optionen

| Antwort einfügen |

| Boardmail an "woblu" |

|

Wertpapier:

Las Vegas Sands

|

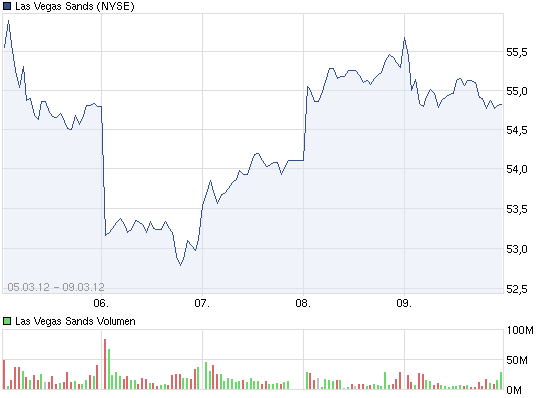

Angeh�ngte Grafik:

chart_week_lasvegassands.png (verkleinert auf 93%)

chart_week_lasvegassands.png (verkleinert auf 93%)

1

14:09 26.03.12

New York (www.aktiencheck.de) - Ryan Worst, Analyst von Brean Murray, Carret & Co, stuft die Las Vegas Sands-Aktie (Las Vegas Sands Aktie) nach wie vor mit dem Rating "buy" ein. Das Kursziel werde von 57,00 USD auf 64,00 USD angehoben. (Analyse vom 26.03.2012) (26.03.2012/ac/a/a)

Offenlegung von m�glichen Interessenskonflikten: Das Wertpapierdienstleistungsunternehmen oder ein mit ihm verbundenes Unternehmen betreuen die analysierte Gesellschaft am Markt. Weitere m�gliche Interessenskonflikte k�nnen Sie auf der Site des Erstellers/ der Quelle der Analyse einsehen.

Quelle: Aktiencheck

Optionen

| Antwort einfügen |

| Boardmail an "Heron" |

|

Wertpapier:

Las Vegas Sands

|

0

http://news.investors.com/article/606727/...ino.htm?ven=yahoocp,yahoo

Am 11. April, Las Vegas Sands ( LVS wird) ge�ffnet sein neuestes Casino in Macau, das Sands Cotai, die sie rufen die weltweit gr��te Tourismus-Projekt ist.

Das Anwesen wird �ber 600 Zimmer und Suiten unter dem Conrad Hotel-Marke, und eine weitere 1200 in einem Holiday Inn verf�gen. Investitionen am Standort Tops $ 8.000.000.000 bisher.

Optionen

| Antwort einfügen |

| Boardmail an "Heron" |

|

Wertpapier:

Las Vegas Sands

|

0

Rating-Aktion

Am 5. April 2012, hob Standard & Poors Ratings Services Corporate Kredit-Rating auf der Las Vegas Sands Corp (LVSC) Familie von Unternehmen zu "BB +"

von 'BB'. Abgesehen von Las Vegas Sands Corp, die LVSC Familie der Nenn Unternehmen beinhaltet Las Vegas Sands LLC, deren venezianische Casino Resort LLC

Tochterunternehmen und Affiliate-VML US Finance LLC (VML). Gleichzeitig wir entfernt alle Bewertungen �ber das Unternehmen aus CreditWatch, wo sie in Verkehr gebracht wurden mit positiven Auswirkungen auf 7. Februar 2012. Der Rating-Ausblick ist positiv.

TEXT-S&P raises Las Vegas Sands ratings

Thu Apr 5, 2012 11:40am EDT

Overview �

-- We believe gaming operator Las Vegas Sands Corp.'s financial

profile has improved to the point that it supports a higher rating, even

incorporating aggressive development spending over time.

-- We are raising our corporate credit rating on Las Vegas Sands to 'BB+'

from 'BB'.

-- We are also revising our recovery rating on the company's U.S. senior

secured credit facilities to '2' from '3' and raising our issue-level rating

to 'BBB-' from 'BB', reflecting the recent redemption of its senior notes.

-- The positive rating outlook reflects our view that further rating

upside is possible based on our current performance expectations, particularly

in the event of a strong ramp-up of Sands Cotai Central.

�

Rating Action

On April 5, 2012, Standard & Poor's Ratings Services raised its corporate

credit rating on the Las Vegas Sands Corp. (LVSC) family of companies to 'BB+'

from 'BB'. Aside from Las Vegas Sands Corp., the LVSC family of rated

companies includes Las Vegas Sands LLC, its Venetian Casino Resort LLC

subsidiary, and affiliate VML U.S. Finance LLC (VML). At the same time, we

removed all ratings on the company from CreditWatch, where they were placed

with positive implications on Feb. 7, 2012. The rating outlook is positive.

�

In addition, we revised our recovery rating on LVSC's U.S. senior secured

credit facilities to '2' from '3'. The '2' recovery rating indicates our

expectation for substantial (70% to 90%) recovery for lenders in the event of

a payment default. Our revised recovery rating follows the recent redemption

of the company's 6.375% senior notes, which shared in the security package

pari passu with obligations under the credit facilities. With the lower amount

of secured debt outstanding, this results in improved recovery prospects for

the U.S. credit facilities under our simulated default scenario.

�

We also raised our issue-level rating on VML's $3.7 billion senior secured

credit facility to 'BB+' from 'BB', reflecting the one-notch rise in our

corporate credit rating.

Rationale �

The upgrade reflects our belief that, under our updated intermediate-term

performance expectations, LVSC will maintain credit measures comfortably

within our threshold for a 'BB+' corporate credit rating, even incorporating

aggressive development spending over time. Given our assessment of LVSC's

business risk profile, we would be comfortable with leverage temporarily

spiking as high as 4.5x to fund development projects, but generally consider

leverage closer to 4.0x to be in line with a 'BB+' corporate credit rating. As

of Dec. 31, 2011, our measure of LVSC's leverage was 3x, which provided a 1x

cushion relative to this threshold, while unrestricted cash balances were

nearly $4 billion. While additional development opportunities, whether in the

U.S. or abroad, will likely take at least a few years to come to fruition, we

expect that LVSC will aggressively pursue them and potentially seek multiple

opportunities at once. Therefore, we view a leverage cushion and large cash

balances as necessary to preserve flexibility in the event opportunities arise

and/or to protect against unexpected performance volatility.

�

The positive rating outlook reflects our view that further rating upside is

possible, based on our current performance expectations. For Las Vegas Sands

to achieve a higher rating (and investment-grade status), we would be

comfortable with leverage temporarily spiking to the high-3x area to fund

development projects, but generally consider leverage closer to 3x in line

with a 'BBB-' corporate credit rating. In the event of a strong ramp-up of

Sands Cotai Central over the next several quarters, we believe an upgrade to

'BBB-' is possible, as we would expect leverage to improve to below 2.5x by

early 2013. An investment-grade rating on Las Vegas Sands, however, would also

require management to publicly articulate a financial policy around its

tolerance for leverage that is aligned with our leverage threshold.

�

Our 'BB+' corporate credit rating on LVSC reflects our assessment of the

company's business risk profile as "satisfactory" and its financial risk

profile as "significant."

�

Our assessment of LVSC's business risk profile as satisfactory reflects the

company's leading presence in the three largest global gaming markets,

high-quality assets and well-known brands, and an experienced management team.

These business strengths are somewhat offset by the gaming industry's

vulnerability to economic cycles given its discretionary nature, the high

levels of competition in the Las Vegas and Macau gaming markets, and

management's aggressive expansion strategy.

�

Our assessment of LVSC's financial risk profile as significant takes into

account the company's large debt burden and track record of adding substantial

leverage to fund development opportunities. Still, notwithstanding these

factors, we expect LVSC's strong liquidity position to allow it to pursue and

finance developments in a manner that preserves credit quality in line with

the current rating. In addition, the company is currently pursuing a

refinancing at its Singapore subsidiary, which will extend debt maturities,

substantially reduce its interest burden, eliminate amortization payments over

the next few years, and increase flexibility to pay cash distributions.

�

Additional risk factors we are monitoring are related to LVSC being subject to

multiple lawsuits and investigations, including the following:

-- An action filed by the former CEO of Sands China alleging the

company's breach of his employment contract and tortious discharge; and

-- An investigation by the SEC and the Department of Justice relating to

compliance with the Foreign Corrupt Practices Act.

�

While the timeframe within which these issues will be resolved is unclear, as

is the extent to which any potential judgment against LVSC would impact credit

quality, these issues may weigh on ratings upside until we have further

clarity around potential judgments or they are resolved.

�

When assessing LVSC's credit quality, we consider the consolidated entity,

despite the distinct financing structures at parent company LVSC and its U.S.,

Macau, and Singapore subsidiaries. We deem the strategic relationship between

the parent and each subsidiary as an important factor that has a bearing on

the credit quality of the overall consolidated entity. However, in notching

our issue-level ratings from the corporate credit rating, we recognize the

distinct financing structures and associated collateral.

�

Our rating incorporates the following specific performance expectations:

-- For LVSC's Las Vegas properties, we are assuming net revenue growth in

the mid-single-digit percentage area in 2012 and 2013. We are also

incorporating an expectation that property EBITDA margin gradually improves to

about 26% in 2013 from 25.2% in 2011. This scenario would result in property

EBITDA growth averaging about 8% per year over this timeframe. This outlook

incorporates our economists' current forecast that growth in U.S. real GDP and

consumer spending will both average about 2% over the next two years. We

believe the Las Vegas Strip should realize at least modest growth in gaming

revenues over this timeframe as the economy continues to gradually improve.

Additionally, Las Vegas visitation trends remain solid, which, combined with

ongoing improvement in group booking levels, should support continued strong

occupancy at LVSC's properties in at least the high-80% area and continued

improved average daily rates during this period.

-- For the Sands Bethlehem property, we are assuming growth in net

revenues and property EBITDA in the high-single digits in 2012, reflecting

continuing benefits from the addition of table games and the recent opening of

the hotel. In 2013, we are assuming more modest growth in both net revenues

and property EBITDA, resulting in EBITDA reaching about $100 million by the

end of 2013.

-- For LVSC's three existing Macau properties, we are assuming a net

revenue decline of 2.5% in 2012, reflecting competitive pressure from Sands

Cotai Central, followed by modest growth in 2013. We are also incorporating an

expectation that property EBITDA margin weakens by approximately 200 basis

points (bps) in 2012 and rebounds slightly 2013, which would result in a

slight decline in EBITDA over the next two years. While growth in Macau has

greatly exceeded our expectations in recent years and we expect the market to

grow in the 10% to 15% range this year, we believe the recently opened Galaxy

resort in Cotai, in addition to Sands Cotai Central, will account for much of

the growth in the Macau gaming market over the next few years. Still, based on

our economists' current forecast that growth in real GDP in the People's

Republic of China will remain in the high-single-digit percentage area over

the next few years, we believe LVSC's existing three properties will benefit

from at least modest revenue growth after 2012 despite substantial new

capacity entering the market. Tourists from China, along with those from Hong

Kong, consistently comprise over 80% of visitation to Macau.

-- For LVSC's Sands Cotai Central development, the rating incorporates a

gradual ramp-up of cash flow as the properties begin their phased opening this

month. Specifically, we have factored property EBITDA of about $250 million

and $440 million in 2012 and 2013, respectively, into our rating.

-- For the Marina Bay Sands property in Singapore, we are incorporating

an expectation for net revenue growth averaging about 5% per year in 2012 and

2013. We are also incorporating an expectation that property EBITDA margin

stabilizes at about 52%, consistent with performance during 2011, which would

result in EBITDA approaching $1.7 billion in 2013. This growth trend is

relatively in line with our economists' current base case forecast for GDP

growth of 5% in Singapore, and also incorporates our view that current hotel

capacity could somewhat constrain growth in 2012 and 2013 (occupancy levels

exceeded 90% in 2011).

�

Based on these performance expectations, we expect consolidated net revenues

and EBITDA to grow approximately 10% in 2012 and 2013. This would result in

consolidate leverage improving to below 2.5x by the end of 2013 and cash

balances in excess of $4 billion.

Liquidity �

Based on the company's likely sources and uses of cash over the next 12 to 18

months and incorporating our performance expectations, LVSC has a "strong"

liquidity profile, according to our criteria. Relevant factors in our

assessment of LVSC's liquidity profile include the following:

-- We expect the company's sources of liquidity over this period to

exceed its uses by 1.5x or more and believe that sources would exceed uses,

even if forecasted EBITDA were to decline by 30%.

-- We believe that LVSC has sufficient covenant headroom under the

proposed new Singapore credit facilities and its existing VML credit

facilities, such that a 30% decline in forecasted EBITDA would not result in a

breach of financial covenants.

-- Covenant cushion relative to the consolidated leverage ratio under the

U.S. credit facilities will tighten over the next several quarters as the

covenant level gradually steps down to 5x by the third quarter of 2012 from 6x

as of Dec. 31, 2011. Still, we are comfortable that LVSC's meaningful excess

cash balances and ability to pay dividends from the Macau and Singapore

subsidiaries (which would be recognized as EBITDA under the U.S. credit

agreement) provide the flexibility to ensure covenant compliance.

�

LVSC derives liquidity from excess cash balances, in addition to revolver

availability and cash generated at its U.S., Macau, and Singapore

subsidiaries. As of Dec. 31, 2011, LVSC had approximately $520 million of

borrowing capacity under the U.S. revolving credit facilities and full

availability under its $500 million Macau revolving credit facility. The

proposed Singapore credit facilities include a Singapore dollar (SGD) 500

million revolver, which will have about SGD 385 million drawn at closing. We

also expect LVSC to benefit from enhanced flexibility to upstream cash

generated in Singapore under the proposed new credit facilities, similar to

its VML facilities. LVSC's ability to move cash from the U.S. entity is

somewhat restricted.

�

During 2011, LVSC generated approximately $2.6 billion in operating cash flow,

which funded about $1.5 billion of capital expenditures, $75 million of

dividends paid to preferred stockholders, and the redemption of the preferred

shares in November 2011. We have assumed aggregate capital expenditures across

the portfolio will approach $3 billion in 2012 and 2013 as the company

completes development of its phased Sands Cotai Central development. This

assumption incorporates some cost overruns with the project. Under our

operating assumptions, expected liquidity is sufficient to fund currently

planned development activity and support covenant compliance without requiring

any further borrowings.

�

Aside from modest amortization payments scheduled under the U.S. credit

facilities, pro forma for the proposed new Singapore credit facilities, debt

maturities in 2012 and 2013 are minimal. Other uses of cash include a dividend

to common shareholders, as the company recently declared a $1.00 per share

(approximately $823 million) annual dividend.

Outlook �

The positive rating outlook reflects our view that a higher rating is possible

over the next several quarters, based on our current performance expectations.

To raise the rating further (into investment-grade status), we would be

comfortable with leverage temporarily spiking to the high-3x area to fund

development projects, but generally consider leverage closer to 3x to be in

line with a 'BBB-' corporate credit rating. In the event of a strong ramp-up

of Sands Cotai Central, we believe an upgrade to 'BBB-' is possible, as we

would expect leverage to improve to below 2.5x by early 2013. An

investment-grade rating on Las Vegas Sands, however, would also require

management to publicly articulate a financial policy around its tolerance for

leverage that is aligned with our leverage threshold at a 'BBB-' rating. In

addition, while the timeframe within which the aforementioned lawsuits and

investigations will be resolved is unclear, as is the extent to which any

potential judgment against LVSC would impact credit quality, these issues may

weigh on ratings upside until we have further clarity around potential

judgments or they are resolved.

�

A revision of the rating outlook to stable or a downgrade could result from

performance meaningfully below our expectations, or from the company taking a

more aggressive posture toward additional development opportunities, resulting

in a sustained spike in leverage to above 4x.

�

Related Criteria And Research

-- Methodology And Assumptions: Liquidity Descriptors For Global

Corporate Issuers, Sept. 28, 2011

-- Criteria Guidelines For Recovery Ratings, Aug. 10, 2009

-- Business Risk/Financial Risk Matrix Expanded, May 27, 2009

-- 2008 Corporate Criteria: Analytical Methodology, April 15, 2008

�

Ratings List

�

Upgraded And Removed From CreditWatch

To From

Las Vegas Sands Corp.

Las Vegas Sands LLC

Venetian Casino Resort LLC

Corporate Credit Rating BB+/Positive BB/Watch Pos

�

VML U.S. Finance LLC

Corporate Credit Rating BB+/Positive BB/Watch Pos

Senior Secured BB+ BB/Watch Pos

�

Upgraded And Removed From CreditWatch; Recovery Rating Revised

To From

Las Vegas Sands LLC

Senior Secured BBB- BB/Watch Pos

Recovery Rating 2 3

�

Ratings Withdrawn

To From

Las Vegas Sands Corp.

Senior Secured NR BB/Watch Pos

Recovery Rating NR 3

Optionen

| Antwort einfügen |

| Boardmail an "Heron" |

|

Wertpapier:

Las Vegas Sands

|

0

19:18 05.04.12

Las Vegas (www.aktiencheck.de) - Die Ratingagentur Standard & Poor’s hat ihre Einsch�tzung f�r den amerikanischen Casinobetreiber Las Vegas Sands Corp. (Las Vegas Sands Aktie) angehoben.

Wie die Agentur am Donnerstag mitteilte, wurde das Kreditrating um eine Stufe von BB auf BB+ erh�ht. Damit wird nun eine Stufe unter Investment Grade eingestuft. Der Ausblick wurde als positiv angegeben.

Als Gr�nde f�r die Rating-Aufstufung nannte Standard & Poor’s die verbesserten Verschuldungskennzahlen, die trotz weiter steigender Investitionen aufrechterhalten werden d�rften. Der positive Ausblick signalisiert, dass innerhalb der n�chsten Quartale eine nochmalige Aufstufung in den Investment-Grade-Bereich m�glich sei.

Die Aktie von Las Vegas Sands notiert an der Nasdaq aktuell bei 58,42 US-Dollar (+2,19 Prozent). (05.04.2012/ac/n/a)

Quelle: Aktiencheck

Google-Anzeigen

Optionen

| Antwort einfügen |

| Boardmail an "Heron" |

|

Wertpapier:

Las Vegas Sands

|

0

Optionen

| Antwort einfügen |

| Boardmail an "Heron" |

|

Wertpapier:

Las Vegas Sands

|

0

Las Vegas Sands Corp Hauptversammlung - 02.00 Uhr EDT -

Optionen

| Antwort einfügen |

| Boardmail an "Heron" |

|

Wertpapier:

Las Vegas Sands

|

0

http://finance.yahoo.com/news/...ands-corp-participate-090000991.html

LAS VEGAS, NV - (MARKET -05/30/12) - Las Vegas Sands Corp ( LVS ) wird in der Sanford C. Bernstein Achtundzwanzigstes Annual Strategic Decisions Conference in New York, NY am Mittwoch, 30 Mai, 2012 teilnehmen. Herr Michael A. Leven, Pr�sident und Chief Operating Officer, wird in einem Kamingespr�ch die voraussichtlich bei ca. 7.00 Uhr beginnen Pacific Time (10:00 Uhr Eastern Time) wird teilnehmen.

Ein Webcast der Diskussion kann durch den Besuch der Investor Relations-Bereich der Website des Unternehmens abrufbar unter www.lasvegassands.com .

�ber Las Vegas Sands

Las Vegas Sands ( LVS ) ist ein Fortune 500 Unternehmen und der weltweit f�hrende Entwickler von Zieleigenschaften (Integrated Resorts), die Premium-Unterk�nfte, Weltklasse-Gaming-und Entertainment-, Kongress-und Ausstellungshallen, sowie Starkoch Restaurants und vielen anderen Annehmlichkeiten ausgestattet.

Das Venetian � und der Palazzo �, Five-Diamond Luxus-Resorts auf dem Las Vegas Strip, und Sands � Bethlehem im Osten von Pennsylvania sind Immobilien der Gesellschaft in den Vereinigten Staaten. Marina Bay Sands � ist das Unternehmen ikonischen Integrated Resort in Singapur, Marina Bay Innenstadt entfernt.

�ber ihre Tochtergesellschaft im Mehrheitsbesitz Sands China Ltd, das Unternehmen besitzt auch ein Portfolio von Liegenschaften, auf Macaos COTAISTRIP �, einschlie�lich der VENETIAN � Macao, Four Seasons Hotel Macao, Cotai und Sands Central, einem 13,7 Mio. Quadratfuss 6400-Zimmer-Integrated Resort Die erste Phase, von denen deb�tierte im April 2012. Das Unternehmen besitzt au�erdem das Sands Macao � auf der Halbinsel Macao.

Las Vegas Sands wird auch zur globalen Nachhaltigkeit durch seine Sande Eco 360-Programm verpflichtet und ist eine aktive Community Partner durch seine verschiedenen karitativen Organisationen.

Kontakt:

Investment-Community:

Sam Levenson

(702) 414-1228

Daniel Briggs

(702) 414-1221

Medien:

Ron Reese

(702) 414-3607

Optionen

| Antwort einfügen |

| Boardmail an "Heron" |

|

Wertpapier:

Las Vegas Sands

|

0

somit steht die Aktie in Europa sehr unterbewertet da, wer hat Informationen über die Zukunft von der ( Termine, Quartal, Aufträge, Erweiterungen, Fusionen) , mal der Service wird jedes Jahr ausgezeichnet gelobt auch mit Preisen überhäuft, ich würde wenn es weiterhin etwas schöner wird in ganz Europa, richtig loslegen mit der, bitte um Informationen?

Grüße

Optionen

| Antwort einfügen |

| Boardmail an "Galindo" |

|

Wertpapier:

Las Vegas Sands

|

0

| 17.06.12 | 15:33 Online Gaming - US-Regulierung könnte noch heuer auf Schiene kommen | boerse-express |

| Die Öffnung des US-amerikanischen Marktes für Online Gaming Anbieter, wie etwa bwin.party, kommt näher: Ein Gesetzesentwurf, der Casino-Spiele im Internet erlaubt, könnte noch vor Jahresende in den US-Kongress gelangen, berichtet die "New York Post" in ihrer Online-Ausgabe. Die Chancen für eine bundesweite Legalisierung von Online Poker und anderen Spiele seien gestiegen, so die Zeitung. Dies sei an einigen Entwicklungen abzulesen: So haben etwa Senate Majority Leader Harry Reid und der Republikaner Jon Kyl in den vergangenen Wochen das Justizministerium ersucht, die Regulierungsbemühungen der einzelnen Staaten zu stoppen. Der Gedanke dahinter: Je mehr Staaten eigene Regelungen schaffen, desto schwieriger wird ein bundesweiter Versuch. Weiters soll Milliardär Sheldo Adelson, Besitzer der Las Vegas Sands Gruppe und ein grosser Unterstützer der Republikaner, nun im Boot für die bundesweite Regulierung sitzen. Er sehe dies als Möglichkeit, seine Umsätze auszuweiten. Dem Unternehmer werden zudem gute Kontakte zu Eric Cantor, dem Mehrheitsführer des Repräsentantenhauses, nachgesagt. Und last but not least soll John Boehner, Sprecher des Repräsentantenhauses, ebenfalls für die Initiative zu gewinnen sein, so die "New York Post". Sein langjähriger persönlicher Berater, Lee Askew, ist heuer zum Vice President of Government Affairs der American Gaming Association ernannt worden. "Die einzige Frage ist lediglich, wie der Gesetzesentwurf im Detail strukturiert sein wird," lässt Roger Gross, Herausgeber des Global Gaming Business Magazins, gegenüber der Zeitung keine Zweifel am Fortschreiten der Iniative offen. Für die Online Gaming Branche geht es um eine Riesen-Markt. |

Optionen

| Antwort einfügen |

| Boardmail an "Galindo" |

|

Wertpapier:

Las Vegas Sands

|

0

kann mir jemand sagen warum die lvs im keller ist ???

Optionen

| Antwort einfügen |

| Boardmail an "Caliber" |

|

Wertpapier:

Las Vegas Sands

|